1. What is the Asia Pacific Emergency Shutdown Systems Market overview, including its definition, scope, and significance?

The Asia Pacific Emergency Shutdown (ESD) Systems market encompasses hardware and software solutions designed to quickly halt operations in hazardous industrial processes, preventing accidents, environmental damage, and loss of life. Scope includes system components such as switches, sensors, programmable safety systems, safety valves, and actuators, deployed across pneumatic, electrical, fiber‑optic, and hydraulic control methods. The market’s significance lies in its critical role in safety compliance for high‑risk sectors like oil & gas, refining, power generation, and chemical manufacturing, driving substantial capital investment and regulatory focus throughout the Asia Pacific region.

2. What are the main drivers, restraints, challenges, and opportunities influencing the Asia Pacific Emergency Shutdown Systems market?

Key drivers include stringent safety regulations, rapid industrialization, and increasing capital projects in downstream oil & gas and power generation. Growth is further propelled by digitalization and the shift toward intelligent, fiber‑optic controls. Restraints arise from high upfront costs and the complexity of retrofitting legacy plants. Challenges involve a shortage of skilled safety engineers and fragmented standards across countries. Opportunities exist in the adoption of predictive maintenance, integration with IIoT platforms, and expanding demand from emerging economies such as Vietnam, Indonesia, and the Philippines.

3. Which current and emerging trends are shaping the growth of the Asia Pacific Emergency Shutdown Systems market?

Current trends feature a move toward modular, plug‑and‑play ESD architectures that reduce installation time. Emerging trends include the integration of advanced analytics, AI‑based fault detection, and cloud‑based monitoring to enhance response times. The adoption of fiber‑optic control methods is accelerating due to superior noise immunity and high‑speed communication. Additionally, sustainability pressures are encouraging manufacturers to develop low‑energy, recyclable components.

4. How has COVID‑19 impacted the Asia Pacific Emergency Shutdown Systems market, and what is the recovery trajectory?

The pandemic caused temporary project delays, supply‑chain disruptions, and reduced capital spending in early 2020. However, health‑related safety awareness amplified the perceived value of robust ESD solutions. By late 2021, project pipelines resumed, supported by government stimulus for infrastructure. Recovery is now robust, with demand rebounding faster than the broader industrial equipment sector, positioning the market for accelerated growth through the forecast horizon.

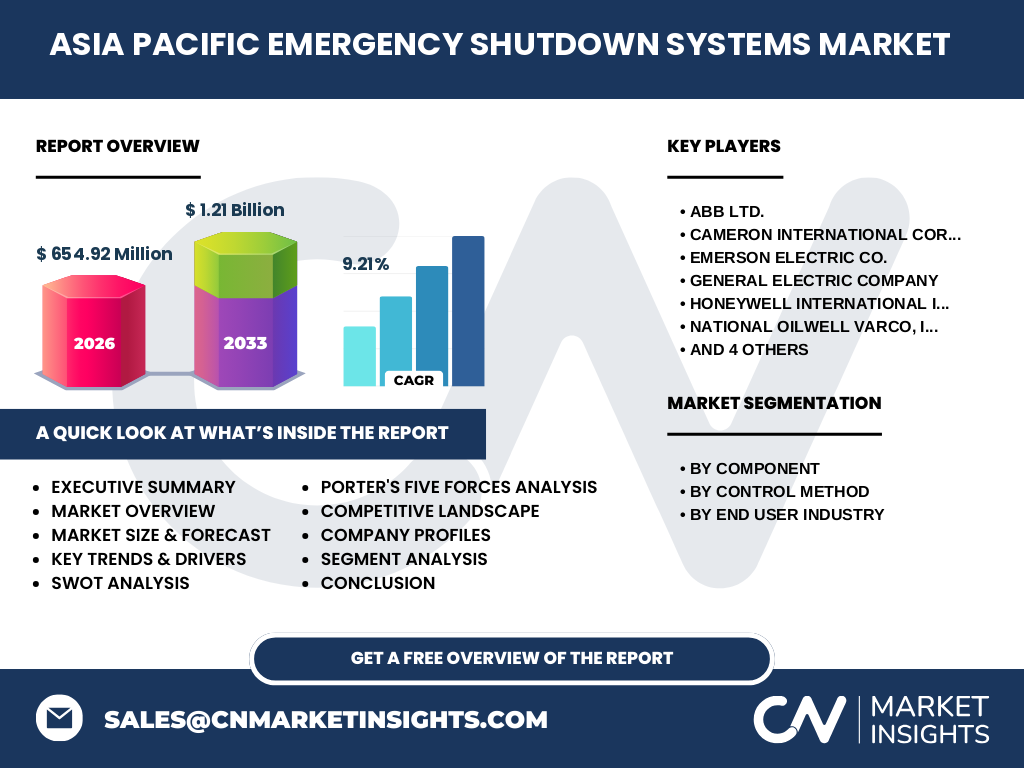

5. Who are the major competitors in the Asia Pacific Emergency Shutdown Systems market, and what does the competitive landscape look like?

The market is dominated by global safety and automation leaders such as ABB Ltd., Emerson Electric Co., Honeywell International Inc., Schneider Electric SE, Siemens AG, Yokogawa Electric Corporation, and OMRON Corporation, alongside specialized providers like Cameron International Corporation, General Electric Company, and National Oilwell Varco, Inc. Competitive dynamics revolve around technological innovation, extensive service networks, and strategic partnerships, leading to moderate consolidation as firms acquire niche technology providers.

6. What are the key findings presented in the executive summary of the Asia Pacific Emergency Shutdown Systems market?

The executive summary highlights a market size of US$654.92 million in 2026, projected to reach US$1.21 billion by 2033, reflecting a robust CAGR of 9.21 %. Growth is driven by expanding petrochemical and power projects, tightening safety standards, and digital transformation. The segmental split shows switches and programmable safety systems leading component demand, while pneumatic and electrical methods retain the largest share of control methods. Regional hotspots include China, India, South Korea, and Australia.

7. What are the market forecasts for the Asia Pacific Emergency Shutdown Systems market from 2025 to 2032?

Based on the provided CAGR of 9.21 %, the market is expected to maintain a steady upward trajectory, moving from the 2026 baseline of US$654.92 million to roughly US$1.21 billion by 2033. This translates into incremental annual growth, with each subsequent year adding approximately US$70‑80 million as new plant constructions, retrofits, and safety upgrades drive demand across all end‑user industries.

8. How is the Asia Pacific Emergency Shutdown Systems market sized and shared by component, control method, and end‑user industry?

By component, the market is segmented into switches, sensors, programmable safety systems, safety valves, and actuators, with switches and programmable safety systems capturing the largest share due to their critical role in initiating shutdowns. Control methods include pneumatic, electrical, fiber‑optic, and hydraulic, where pneumatic remains dominant, followed by electrical, while fiber‑optic gains momentum. End‑user industries are oil & gas, refining, power generation, and chemical, with oil & gas and power generation accounting for the bulk of deployments.

9. What is the geographic distribution of the Asia Pacific Emergency Shutdown Systems market size and share?

The market’s geographic footprint spans China, India, Japan, South Korea, Australia, and Southeast Asian nations. China and India together represent the largest share, driven by extensive upstream and downstream projects. Japan and South Korea contribute significant volume through advanced manufacturing and high‑tech adoption, while Australia’s strong mining and LNG sectors add to regional diversity. Southeast Asia offers high growth potential as new petrochemical parks emerge.

10. What are the detailed regional performance insights for the Asia Pacific Emergency Shutdown Systems market?

China leads in absolute value, benefitting from massive refinery upgrades and offshore platform expansions. India shows rapid growth, propelled by new power generation capacity and offshore exploration. Japan’s market is characterized by premium, high‑reliability solutions for existing mature plants. South Korea focuses on advanced automation integration, while Australia’s market is driven by LNG export facilities. Southeast Asian economies, notably Indonesia and Vietnam, are early‑stage but exhibit strong CAGR due to greenfield projects.

11. Which leading companies operate in the Asia Pacific Emergency Shutdown Systems market, and what are their strategic approaches?

ABB Ltd. leverages its digital Twin and Ability platform to offer smart ESD solutions. Emerson emphasizes its DeltaV safety system suite and extensive field service network. Honeywell focuses on integrated safety and cybersecurity offerings. Schneider Electric promotes EcoStruxure for connected safety. Siemens combines its S7 automation portfolio with robust safety modules. Yokogawa highlights its FAST/ESD controllers. OMRON drives compact, sensor‑rich designs, while Cameron International and National Oilwell Varco provide niche valve and actuator expertise.

12. How does Porter’s Five Forces analysis describe the competitive environment of the Asia Pacific Emergency Shutdown Systems market?

Threat of new entrants is moderate; high capital requirements and regulatory barriers deter newcomers. Bargaining power of suppliers is low to moderate, as component suppliers are abundant, but specialized sensor manufacturers hold some leverage. Bargaining power of buyers is moderate; large industrial clients negotiate pricing and demand comprehensive service contracts. Threat of substitutes is low, given the safety‑critical nature of ESD systems. Industry rivalry is high, driven by innovation, service quality, and geographic reach.

13. What are the SWOT points for the Asia Pacific Emergency Shutdown Systems market?

Strengths: Essential safety function, strong regulatory backing, and high technological entry barriers. Weaknesses: High upfront costs and complex integration with legacy plants. Opportunities: Digital integration, AI‑based diagnostics, and expansion into emerging economies. Threats: Economic slowdown affecting capital projects and potential supply‑chain disruptions for critical components.

14. How is the value chain of the Asia Pacific Emergency Shutdown Systems market structured?

The value chain starts with raw material suppliers (electronics, steel, plastics), moves to component manufacturers (switches, sensors, valves, actuators), followed by system integrators that assemble and program the ESD solutions. Distributors and system integrators provide regional sales and installation services. After‑sales support, maintenance, and periodic testing form the final stage, ensuring compliance and system reliability throughout the equipment lifecycle.

15. What investment insights can be drawn for stakeholders interested in the Asia Pacific Emergency Shutdown Systems market?

Investors should target companies with strong digital portfolios and proven service networks across China, India, and Southeast Asia. Opportunities exist in joint ventures that combine local market knowledge with global technology. Funding R&D in fiber‑optic controls and AI‑driven analytics can yield high returns, given the market’s 9.21 % CAGR. Additionally, acquiring niche actuator or valve specialists can enhance product breadth and create cross‑selling channels.

16. What are the key conclusions from the Asia Pacific Emergency Shutdown Systems market analysis?

The market is on a clear growth path, underpinned by regulatory imperatives and a surge in industrial projects across the region. With a projected value of US$1.21 billion by 2033 and a healthy CAGR, firms that innovate in digital safety, expand service capabilities, and tap emerging economies will capture the most value. The competitive landscape remains intense, emphasizing the need for differentiation through technology and customer support.

17. How was the research for this report conducted?

The study employed a blend of primary interviews with industry experts, OEM engineers, and safety consultants, complemented by secondary data from company filings, regulatory publications, and reputable market databases. Quantitative forecasts used historical growth patterns, the supplied CAGR of 9.21 %, and scenario analysis to validate the 2026 baseline of US$654.92 million and the 2033 projection of US$1.21 billion.

18. What is the scope of this research, and what limitations should readers be aware of?

The scope covers the Asia Pacific region, focusing on component, control method, and end‑user segmentation, and includes major OEMs and system integrators. Limitations arise from the reliance on publicly disclosed data and the exclusion of confidential contract values. While the forecast reflects macro‑level trends, micro‑level project delays or policy shifts could affect individual country performance.

19. Which key companies have recent developments, and what are their latest product launches or partnerships in the Asia Pacific Emergency Shutdown Systems market?

ABB recently launched its Cloud‑connected ESD suite for offshore platforms in Singapore. Emerson introduced a new programmable safety system with integrated AI diagnostics in India. Honeywell announced a partnership with a leading Indian refinery to retrofit its emergency shutdown architecture with cyber‑secure controllers. Schneider Electric unveiled a fiber‑optic sensor line aimed at high‑speed shutdown in Japanese petrochemical plants. Siemens signed a strategic alliance with an Australian LNG operator to deploy modular ESD blocks across new export terminals.